The “Bidenomic Boom”

Genevieve Signoret & Delia Paredes

(Hay una versión en español de este artículo aquí.)

We continue to share excerpts from our September 11 report, Quarterly Outlook 2023–2025: Soft Landing Yet Again, where we present three scenarios for the global economy over the next two years. You can think of our scenarios as train tracks: each takes the economy in a different direction. A scenario is built on a group of assumptions. Our three sets of assumptions “pivot” the economy from one track to another.

“Bidenomics” is a catchword for the Biden administration’s approach to economic policy: strong fiscal stimulus during the pandemic, investments in infrastructure, investments to accelerate the country’s energy transition, a strengthening of the safety net, a minimum wage hike, expanded access to affordable healthcare, and expanded worker training, all purported to be paid for with tax increases on high-income individuals and corporations. The administration sells Bidenomics by contrasting it to the trickle-down approach based on tax cuts which, it says, has caused inequality.

Lately, the term “Bidenomics” has been associated above all with the so-called Inflation Reduction Act of 2022 (IRA), which appropriates billions of dollars in loans, credit subsidies, and loan guarantees for innovation and infrastructure related to transitioning to clean energy.

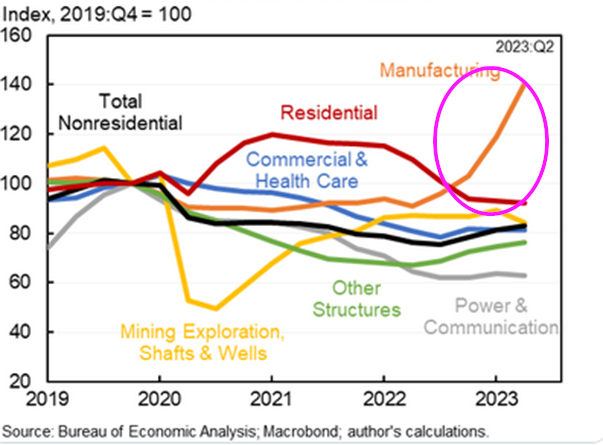

The term “Bidenomic Boom” is our own. It refers to a recent burst of construction in the manufacturing sector seen by analysts to be a possible first sign of an IRA impact.

Bidenomics?

US private-sector investment in structures

Our source is Jason Furman on Twitter.

What no one knows is whether this boom will prove lasting, or whether it will have strong positive spillovers. We assume in our central scenario that over the next eight quarters its “volume” (strength) will crescendo a bit, and that it will indeed have some positive spillovers and be sustained.

In our forecast, this assumption drives the fact that the U.S. economy does not slide all the way down into recession but rather lands softly.