Full Forecast for Mexico in 2024–2025

Delia Paredes & Genevieve Signoret

(Hay una versión en español de este artículo aquí.)

You can read the main takeaways here, the full report here, and consult our forecast tables here.

Momentum

Inflation in Mexico ended 2023 at 4.7%, down from 7.8% in 2022 on account of slower inflation in consumer goods. Goods inflation slowed to 4.9% in 2023 from 11.1% the year before, while service inflation at 5.3% remained practically unchanged from 2022.

With overall inflation in decline, Banxico, which has kept its monetary policy rate at 11.25% for almost 12 months, is fairly confident that inflation will converge to its target by the end of 2025 so has signaled that it will consider cutting rates as early as March. At the same time, Banxico is cautious. Even if it does cut its rate in March, it will likely convey to markets that the cut should not be construed as the start of a rate-cutting cycle. It intends to hold a restrictive stance.

Economic activity continues to be supported by private investment in preparation for nearshoring and pre-electoral accelerated public investment in President López Obrador’s flagship programs. All this investment spending has in turn boosted private consumption.

On the other hand, growth in 2023 ended with weaker momentum than we had expected. The slowdown last quarter was broad. Construction continued to grow at a fairly strong pace but its share in GDP growth shrank. Private consumption, too, kept up its fairly rapid expansion, supported by wage increases, cash transfers from social programs, and pre-electoral spending.

The Mexican peso ended 2023 at 17.18 pesos per dollar, supported by the interest rate differential with the United States and bullish views on the Mexican economy on the part of international investors.

Three Scenarios

In all three of our scenarios for the Mexican economy, fiscal policy is expansionary in 2024 and tight in 2025; and Banxico loosens its monetary stance.

Expansionary fiscal policy in 2024 and restrictive in 2025

According to the fiscal package approved by Congress, the deficit will go from 3.9% to 5.4% in 2024, and then to 2.6% in 2025. This implies that the fiscal boost to growth from elections will dissipate next year. Moreover, in the first year of every new administration, spending tends to slow down, as new officials learn to execute.

Weaker monetary restriction

Given inflation dynamics, we think that in March the central bank will feel it can carry out a “hawkish cut”—a rate cut in which the bank signals an intention to subsequently pause rather than proceed with an easing cycle.

Likewise, we think that 2024 will bring two regimes, one prior to the elections and the other afterwards. In the first regime, growth will be driven by pre-electoral spending and vigorous demand from the United States. In the second phase, growth will moderate, as the effects of electoral spending quickly fade away and the U.S. economy slows down.

Global influence

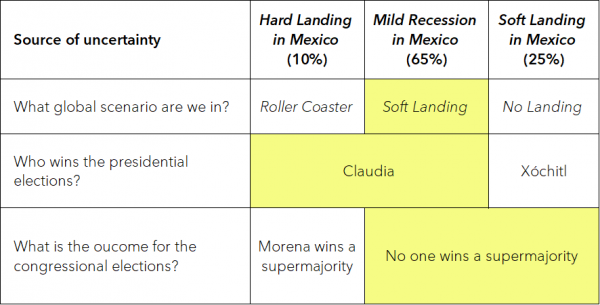

Two factors distinguish our scenarios for the Mexican economy: international conditions (growth, inflation, and rates) and the outcome of Mexican elections.

As we note in Global Outlook 2024–2024: No Landing?, we’ve built three scenarios for the global economy:

- No landing (probability: 55%), in which activity in the United States slows down some in the second half of 2024 before reaccelerating.

- Soft Landing (35%), in which activity in the United States slows down sharply in the second half of 2024 before reaccelerating.

- Roller Coaster (10%), in which economic activity in the United States strengthens in 2024, generating a bout of inflation that triggers a rate hike, which in turn leads the economy into a recession in 2025.

Electoral outcome

Even more than assumed external conditions, what distinguishes our three scenarios for Mexico is our assumptions as to the composition of Congress after the June 2 elections. The most likely outcome is that no coalition will manage the congressional supermajority it needs to amend the Constitution. But we cannot rule out a scenario in which Morena and its allies do achieve such a supermajority, either on their own or by cobbling one together with members of the opposition who, hoping for positions of power, jump ship.

Summary of scenarios for Mexico

Combining our assumptions as to external economic conditions with internal political outcomes, we have the following set of pivotal assumptions:

Assumptions that distinguish between scenarios for Mexico

Source: TransEconomics.

Forecast

Mild Recession in Mexico (subjective probability = 65%)

Mild Recession in Mexico is our central scenario for Mexico. It corresponds to our Soft Landing scenario for the global economy. We assign to it a subjective probability of 65%.

In Mild Recession in Mexico, the status quo is maintained after the Mexican election: Claudia Sheinbaum, the Morena candidate, wins. But Morena and its allies fail to build a supermajority in Congress. Both the current agenda of constitutional reforms and Sheinbaum’s own agenda face significant obstacles.

The U.S. economy maintains its pace of growth in the first half of the year before moderating in the second half. This allows the Mexican economy to grow at a clip of approximately 3% in the first half of 2024. Mexican economic activity continues to benefit from not only external demand but also tailwinds pushing on private consumption, although the impetus from gross fixed investment does weaken.

In the second half of the year, momentum weakens to an average annual growth rate of around 2%, on weaker electoral spending and gross fixed investment both. The economy contracts in the last quarter of 2024 and the first quarter of 2025, in a technical recession. Because of weaker external demand and the effects of a restrictive fiscal policy, growth in the following year remains anemic.

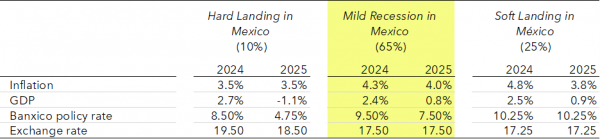

Mexico’s growth in 2024 is 2.4%, and in 2025, 0.8%.

Inflation continues its downward trend to end 2024 at 4% and finally falls within Banxico’s target range to close 2024 at 3.8%.

These inflation results allow Banxico to start cutting rates in tandem with the Fed. The Fed starts cutting in June and ends the cycle in June 2025 for a terminal rate of 7.5%.

The Mexican peso follows its usual path for an election year, weakening to around 18.50 pesos per dollar but bouncing back to 17.50 after the election. Next year, given Banxico’s rate-cutting cycle, the exchange rate reaches 19.00 pesos per dollar and closes the year at around 18.00. Neither the U.S. electoral process nor its outcome has a significant impact on the exchange rate.

Soft Landing in Mexico (25%)

Soft Landing in Mexico corresponds to our No Landing scenario for the global economy. We assign a subjective probability of 25% to this scenario.

The opposition candidate, Xóchitl Gálvez, wins the presidency but fails to obtain a supermajority in Congress. Neither Morena nor Gálvez is able to amend the Constitution.

Economic activity receives an additional boost from external demand, expanding 2.5% in 2024, and manages to avoid a recession in 2025 (estimated growth: 0.9%). The growth outlook improves substantially thanks to the electoral outcome. A victory by Gálvez stimulates an even more positive narrative regarding nearshoring, the energy sector, and trade relations with the United States and Canada.

As in the central scenario, in this one, inflation continues its downward trend and ends 2025 within Banxico’s target range, although in both years inflation ends at slightly higher rates than in the central scenario. This allows Banxico to start a rate-cutting cycle in tandem with the Fed in June and ends in December 2024 with a terminal rate of 10.25%.

The Mexican peso follows its usual path for an election year, weakening to around18.00 pesos per dollar but returning to 17.50 after the election. In this best of all three scenarios for external perceptions of Mexico country risk, the exchange rate ends 2025 not far from its current level, at 17.25.

Hard Landing in Mexico (10%)

Hard Landing in Mexico corresponds to our Roller Coaster scenario for the global economy. We assign a subjective probability of 10% to this scenario.

In Hard Landing in Mexico, Claudia Sheinbaum wins the elections and manages to build a supermajority in Congress. The current proposed reform agenda passes, and the new president has no problem pushing through her own agenda. The business climate in Mexico deteriorates significantly.

The economy in the United States is more dynamic during the first three quarters of the next year than in the central scenario. But it suddenly slows down at the end of 2024, leading to a growth rate for the entire year in Mexico of 2.7%. In 2025, the recession in the United States as well as the electoral outcome in Mexico cause a deeper recession than in the central scenario. Mexican GDP contracts by 1.1%.

In this scenario, inflation hovers around 4.9% for most of next year on rapid core inflation driven by persistent upward demand-side pressure. In 2025, inflation slows to 3.6%. The central bank conducts a much more aggressive rate-cutting cycle, reducing the rate differential with the United States to 325 basis points from its current 550. Consequently, the exchange rate increases after the election to 19.50 towards the end of the year, where it stays for most of 2025.

Our three scenarios, summarized

Source: TransEconomics.

You can find our full forecast tables here.