Incoming Data and Events So Far Confirm No Landing

Genevieve Signoret & Delia Paredes

(Hay una versión en español de este artículo aquí.)

By our reading, data that have come in since our last edition of Quarterly Outlook has confirmed our base case for the global economy, No Landing. And, with a couple exceptions, have roughly aligned with our forecasts.

A mild slowdown

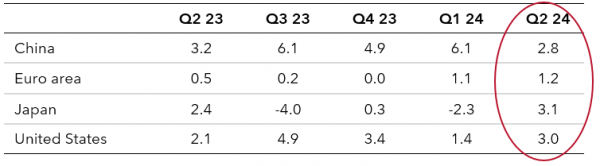

The exceptions were quarter-two U.S. and euro-area growth. Contrary to our expectations, last quarter, GDP growth did not slow down in the United States or the euro zone.

Second-quarter growth in China and Japan did match our June estimates, slowing down sharply in China and accelerating in Japan.

Q2 GDP growth in the United States and the euro area proved stronger than we anticipated. In Japan and China, it was roughly in line.

Gross Domestic Product (seasonally adjusted annual rate %)

Source: Bloomberg

What about the current quarter?

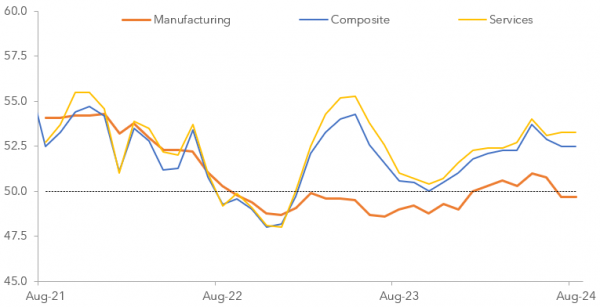

Overall, high-frequency data this quarter suggest that the global economy is undergoing a mild slowdown consistent with No Landing.

Global PMIs suggest a mild slowdown in Q3 consistent with our No Landing base case

Global Purchasing Manager Indices (Diffusion indices)

Source: Bloomberg

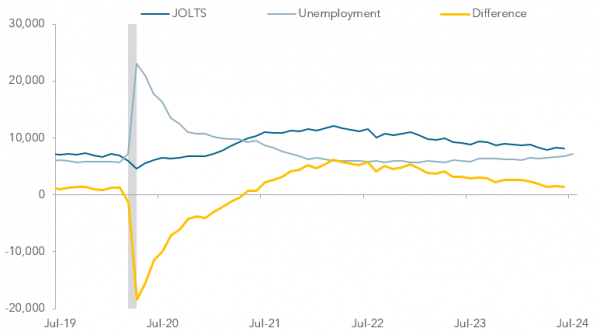

A few labor numbers scared markets but not us

The July U.S. jobs report showing only 114,000 new jobs when the market consensus had been 175,000 startled markets in August. Subsequent unemployment data, however, calmed markets down.

We didn’t need calming down. As Dario Perkins of TS Lombard explains here, Covid distorted the U.S. job market, opening up an unusually wide gap between the supply and demand for labor. This gap is now closing. Hence, we see labor market numbers that in a normal business cycle would be a legitimate cause for concern likely to signify a mere restoration of normality.

Notwithstanding the July jobs report, in recent U.S. labor market data, we don’t see signs of a looming recession. Or even a soft landing.

USA: Job Openings and Labor Turnover (dark blue), Unemployed workers (light blue), and the gap between them (orange), in thousands

Source: St. Louis FRED

We could be wrong of course! That’s why we have more than one scenario.

Disinflation continues outside of Japan

Consumer price data has confirmed our June view that, outside of Japan, disinflation will continue.

Global disinflation continues on trend (outside of Japan)

Inflation in selected countries, % annually

Source: Bloomberg

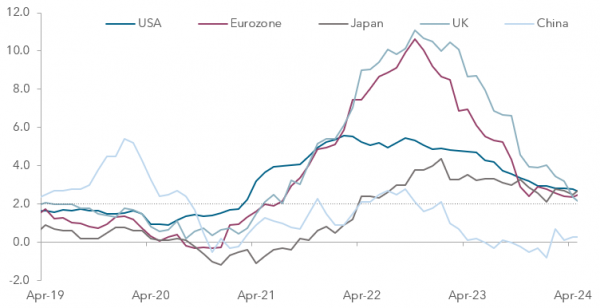

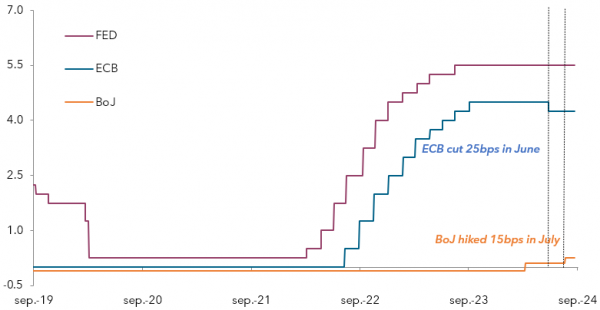

And central banks outside of Japan have begun to loosen

Not only have incoming growth, jobs, and inflation confirmed No Landing by our reading, but also they have triggered the responses we foresaw in central-bank decisions and communication.

The European Central Bank apparently saw the May uptick in the euro area’s annual rate of inflation as a blip and on 6 June began what we believe will be a sustained loosening cycle with an initial quarter-point cut.

The Federal Reserve Open Market Committee did not follow suit in July but has clearly signaled intentions to do so in September.

The Bank of Japan, meanwhile, confident that the country is finally exiting deflation, on 31 July hiked rates by 15 basis points to 0.25%.

As expected, in recent months, the ECB has cut its policy rate, Japan has hiked, and the U.S. has signaled intentions to cut soon

Monetary policy rates, %

Source: Bloomberg

In sum, we continue to see it likely that the global economy is on and will remain on a path consistent with our base case, No Landing.

TransEconomics delivers serenity to high–net-worth families and individuals. To learn more, request an appointment with an advisor.