How Did We Do?

Genevieve Signoret & Delia Paredes

(Hay una versión en español de este artículo aquí.)

Accountability pushes us to improve, so we report here how we did on our last set of base-case global macro projections for the third quarter of this year.

Growth

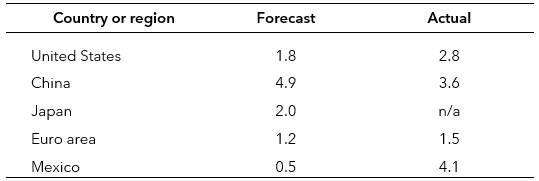

Whereas China grew more slowly in quarter three than we had anticipated in our base case, the United States, the euro area, and, especially, Mexico, grew more quickly.

How did we do in our growth projections?

GDP in 3Q24, quarter-on-quarter % ch, saar

Source: TransEconomics, Bloomberg.

In the case of the United States, we underestimated consumer demand resiliency. In the case of Mexico, we await the demand-side breakdown of GDP figures to see where the unexpected surge came from.

Inflation

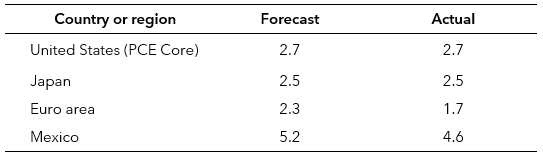

Our outlooks as to the pace of disinflation in the euro area, and, especially, Mexico, were overly pessimistic.

How did we do in our inflation projections?

Consumer Price Index (Sep 2024), 12-month % change

Source: TransEconomics, Bloomberg.

In the euro area, weaker-than-expected consumer demand drove the unexpected slowdown in inflation.

In Mexico, September educational services and fresh food prices turned out lower than we had been expecting.

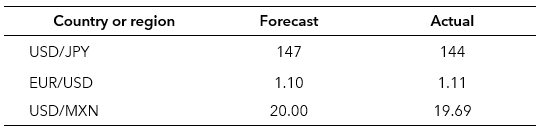

Monetary Policy Rates, Yields and Exchange Rates

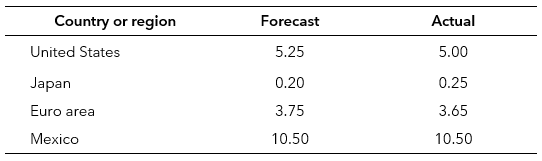

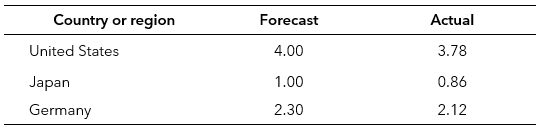

Monetary policy rates, yields on 10-year government bonds, and exchange rates came in largely in line with our expectations. Our biggest miss was for the yield on a 10-year Japanese government bond, which ended September below our projected 1.00% at 0.86%.

How did we do on monetary policy?

Monetary policy rate (Sep 2024), % per annum

Source: TransEconomics, Bloomberg.

How did we do on long-term government bond yields?

Yield on a 10-year Govt Bond (Sep 2024), % per annum

Source: TransEconomics, Bloomberg.

How did we do on exchange rates?

Source: TransEconomics, Bloomberg.

TransEconomics delivers serenity to high–net-worth families and individuals. To learn more, request an appointment with an advisor.