Mexico 2025 Budget Package Is Not Credible

Delia Paredes & Genevieve Signoret

(Hay una versión en español de este artículo aquí.)

On November 15, Claudia Sheinbaum’s administration presented its first budget package to Congress. Covering the upcoming year, it includes the proposed Revenue Law, General Economic Policy Guidelines, and the Expenditure Budget. Congress has until December 15 to approve it.

We see the package as conservative but ridden with implementation risks. It’s not entirely credible, thus it poses risks to stability.

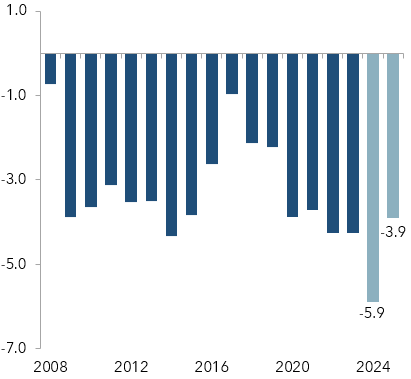

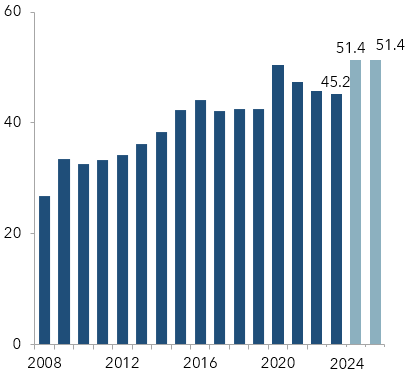

As expected, the government proposes reducing the fiscal deficit by two percentage points of GDP, rather than the three points it announced last April. This would hold debt to 51.4% of GDP and bring about a primary surplus of 0.6% in 2024. Thus, it’s meant to demonstrate the new administration’s commitment to fiscal discipline in the medium term.

The budget proposal would reduce the deficit by 2 percentage points of GDP while maintaining a constant debt-to-GDP ratio

|

Government deficit1, % of GDP |

Total debt, % of GDP2 |

|

|

|

|

|

Source: SHCP. |

||

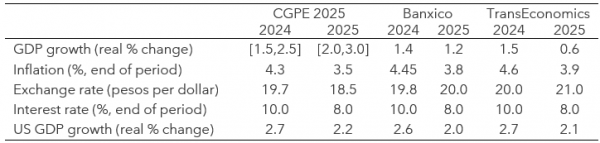

At first glance, the plan looks sound. But it relies on rather optimistic assumptions. According to the government, the economy will grow by 2% in 2024, accelerating to 2―3% in 2025. But these figures are far more optimistic than market projections and those of TransEconomics.

The package assumes, further, an exchange rate of 19.70 pesos per dollar by end-2024 and 18.50 by end-2025—rates that also differ greatly from what other analysts anticipate.

Oil assumptions look rosy as well. For example, Pemex is assumed to export 900,000 barrels per day in 2024 and 892,000 in 2025. These numbers contrast with this year’s daily average of 788,000.

Sunny budget assumptions pose two risks. The first and more obvious is the risk of spending cuts later on to meet the projected fiscal balance. This risk is particularly pronounced in Mexico today, where fiscal room to maneuver is scarce.

The second concerns credibility. If market participants don’t view the government’s model assumptions as credible, to be persuaded to keep funding the government, they may start to demand higher risk premia. Funding costs then rise, and the local currency weakens. This, in turn, renders the budget projections less realistic still, triggering a vicious cycle that can ultimately escalate into a crisis.

The budget was formulated under assumptions we see as overly optimistic

Macroeconomic variables

Source: SHCP, Banxico Survey (October 2024), TransEconomics.

On the revenue side, the budget package assumes that, thanks to technological modernization, the Treasury will achieve greater efficiency in collecting non-oil taxes. The plan does not propose major changes to the tax framework but does include adjustments to certain fees and duties.

On the spending side, the package outlines a plan to cut programmable spending by 1.8 percentage points of GDP, including a 0.9-point reduction in capital expenditures. Such a cut would curb domestic demand. But the budget proposal projects domestic demand so robust that it drives growth rates up.

The package leaves the government with scarcely any room to respond to an unforeseen crisis. In fact, non-discretional spending such as debt service, pension payments, and state-owned enterprise expenditures, account for as much as 80% of the budget total.

The plan proposes that Pemex and CFE maintain financial discipline. Its target for Pemex is a financial surplus of 249 billion pesos, to be achieved via a government transfer and an “Oil Rights for Welfare” royalty to replace royalties on exports and extraction and the DUC profit sharing rate. This would cap the overall Pemex fiscal burden at 30%.

These targets for state-owned enterprises, however, appear to conflict with recently announced plans for greater investment in infrastructure and production in the energy sector. We see tension between the goals of reducing the deficit and plans to invest in strategic sectors.

With Moody’s recently having changed its Mexico sovereign debt outlook to negative, implementation risk for this budget package looms large. If revenues fall short of projected levels, or financial support to Pemex needs to be expanded—become more explicit or entail greater resources—the risk of a sovereign credit rating downgrade will rise.

TransEconomics delivers serenity to high–net-worth families and individuals through holistic wealth management and international alternative asset management. To learn more, request an appointment with an advisor.